Tadalafil zeichnet sich durch eine außergewöhnlich lange Halbwertszeit im Vergleich zu anderen PDE5-Inhibitoren aus. Diese pharmakokinetische Eigenschaft führt zu einer verlängerten Exposition des Wirkstoffs im Organismus. Die Eliminationsrate hängt von der hepatischen Aktivität des CYP3A4-Enzyms ab. Lipophile Eigenschaften unterstützen eine weite Verteilung in unterschiedlichen Geweben. Eine ausgeprägte Stabilität gegenüber Nahrungsaufnahme macht den Stoff besonders konstant in seiner Wirkung. Unter generischen Präparaten wird cialis online häufig mit einem vergleichbaren pharmakologischen Profil beschrieben.

2010_book_review_capitalism_needs_foresight

Emerald | The Trouble with Markets – Saving Capitalism from Itself

The Trouble with Markets – Saving Capitalism from Itself Article Type: Book review From: foresight, Volume 12, Issue 4 Roger Bootle, Nicholas Brealey Publishing, London, 2009, 276 pp.

Capitalism needs foresight!

Bootle’s book has three parts each with three chapters and a conclusion titled The Future of Capitalism with 169 footnotes:

Part I: The Great Implosion – reports on the development of the crisis.

Part II: The Trouble with Markets – examines the deep causes of the crisis.

Part III: From Implosion to Recovery – is devoted to cures.

The title of the conclusion chapter, The Future of Capitalism, actually qualifies the book for a review in this journal.

As someone active in the financial sector for 30 years, the author’s background identifies him as a possible knowledge source in trying to understand the turmoil of 2007-2009. According to the author, the book is the third part of a trilogy:

[…] in the process of addressing the major questions about the future of the market economy, the book also attempts to build on my earlier work […] and argues that, despite huge risks and challenges, the low inflation era will last a good many years yet. Although the book does have things about the immediate economic outlook, this is not a book of forecasts …

[…] my first book published in 1996 […] argued that the world faced a future of low inflation accompanied by high rates of economic growth and low unemployment. What the first book did not foresee was that as the forces that produced low inflation gathered strength, darker clouds would appear, partly as a direct result.

[…] the weakness of the second book, published in 2003, was not that it failed to foresee future events, but rather that it failed to see their full ramifications.

In the book, Bootle examines the origins of the 2007/2009 financial crisis through a certain lens. I would have expected from him to have more statistics, tables and figures in the chapters, so that the readers can have a feeling of the size of the capitalist world along different dimensions. In the following paragraphs, I will try to do this.

Capitalist order

Bootle’s book is interesting in that it seems to criticize capitalism of 2007-2009 and of earlier periods, but in reality, it actually defends it. The author praises self-interest, but then complains about the lack of social responsibility (page 73). With certain arguments, the author actually blocks all criticism of Capitalism: “[…] the market is a human construct, and humanity is flawed” (page 92), “fraud is especially prevalent in

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Emerald | The Trouble with Markets – Saving Capitalism from Itself

financial markets because of […] genuine uncertainty about the future […]“ (page 117). Mitchell (1914) had brought up human nature from a different perspective, “[…] it is possible that the effort to keep the study of human nature out of economic theory may break down. The admitted deficiencies of hedonism may stimulate future economists […] to look for sound psychological analysis […] Human nature is in large measure a social product […]” and drew conclusions for research.

Schumpeter (1928) was more courageous “[…] I shall deal merely with the question whether or not the capitalistic system is stable in itself – that is to say, whether or not it would, in the absence of such disturbances (i.e., disturbances arising from without the sphere of economic life), show any tendency towards self-destruction from inherent economic causes, or towards out-growing its own frame […] when we merely mean to speak of the question of what may be termed the institutional survival of capitalism, we will henceforth speak of the capitalist order instead of the capitalist system. When speaking of the stability or instability of the capitalist system, we shall mean something akin to what business men call stability or instability of business conditions. Of course, mere instability of the ‘system’ would, if severe enough, threaten the stability of the ‘order’, or the ‘system’ may have an inherent tendency to destroy the ‘order’ by undermining the social positions on which the ‘order’ rests.”. Sounds familiar!?

Fifty-seven years later, (in an effort “to save capitalism from itself ”!), a US Senator (Gore, 1985) introduced a bill that would establish an Office of Critical Trends Analysis within the Executive Office of the President. Its mission would be to advise the president, and the country, “of the potential effect of government policies on critical trends and alternative futures”. He was trying to stop the government from “thinking that it is wise to spend tomorrow’s money today to solve the problems of yesterday”.

PONZI Scheme, speculation and crisis

Although Bootle fails to state openly that the dominant economic system of the world, i.e. Capitalism, is a Worldwide PONZI Scheme, he must be credited for writing “[…] the whole financial system was a gigantic inverted pyramid of debt, resting on a tiny base of capital” (page 11). The Economist (2009) is more blunt and calls the USA “a Ponzi scheme that works”.

Bootle’s anger towards the academia (page 21) is very intriguing. Several members of the academia in different fields have been trying to understand the world for centuries. The author should know better that all models (e.g., rational expectations, efficient markets, etc.) are idealization of real world experiences and are, by definition, incomplete and wrong, as briefly discussed in Watling (1964). It is up to the individual to use the models in an appropriate and legitimate way. I must admit that some members of the Western academic world have been legitimizing this scheme with their “so-called scientific” research work. In a microeconomics textbook (Gottheil, 1999), one finds that a worse income distribution (income inequality as measured by Gini coefficent) is better for the poor in the long run, although in the long run we are all dead!

The author is very skillful in putting the blame for any rising problem not onto the shoulders of the dominant economic and financial system, i.e. Capitalism, but on the individual misbehaviors, be it investors, professionals, rating agencies, regulators, politicians and ordinary citizens. Henninger (2009a) calls these behaviors “cataclysmic behaviours”. Although we read many examples of companies being mugged by their executives, members of the Worldwide PONZI Scheme defend them with the following argument “Honoring contractual commitments is at the heart of what we do in the insurance business” (Henninger, 2009b), as does Bootle.

The Worldwide PONZI Scheme has supporters in every country of the world. If there aren’t any, the system creates them by pushing the virtues of globalization and foreign (or global, which is the preferred term) capital, a necessary ingredient for indefinite (?!) and limitless (?!) growth. The author uses this approach to criticize China in Chapter 6. He calls on China to save Capitalism, better, to save USA and other Western developed countries. It is rather strange that he blames China for the turmoil: “[…] this disaster was made in China […]” (page 21).

Although the author touches upon the excesses of Western capital, he avoids discussing its disequilibrating effects, e.g., capital inflows of US$135 billion into Russian Federation in 2007 and capital outflows of US$85 billion from Russian Federation in 2008. As the system feeds itself on disequilibrium, each and every disequilibrium creates its own legal PONZI scheme. Examples of this “pump in - suck out” scheme can be found using World Bank data.

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Emerald | The Trouble with Markets – Saving Capitalism from Itself

Short selling of equities is another form of legal PONZI Scheme. Kessler (2009) explains: “In an typical bear raid, traders short a target stock – i.e., borrow shares and then sell them, hoping to cover or replace them at a cheaper price. Once short, traders then spread bad news, amplify it, even make it up if they have to, to get a stock to drop so they can cover their short.” In their effort to create “their desired future”, traders create turmoil, which brings up the discussion of “intention and foresight in criminal law” used to distinguish between murder and manslaughter (Oberdiek, 1972).

If intentions are bad, no regulation can stop the bad behavior, as Gort and Wall (1988) have shown that the feedback from investor expectations to regulatory behavior, together with investor expectations (with both perfect and imperfect investor foresight) that take account of this feedback, basically alters the consequences of regulatory decisions. Steigerwald and Stuart (1997) have also shown that “current investment appears to reflect currently information but little foresight other than foresight of enacted policy changes”.

In 1902, 102 years ago, Selden (1902) analyzed speculative behavior by dividing the society into five groups, arranged according to the degree to which business transactions are affected by the effort to speculate:

Those who work for wages and buy only for consumption. The attempts of this class to foresee and profit by changes in value are for the most part sporadic and without important influence.

Those who work independently, like small farmers and shop-keepers. In the USA this represents a large portion of the population, includes some of the most persistent speculators.

Entrepreneurs. Others may speculate; but the entrepreneur, seeking to steer a profitable course between Scylla of expenses of production and the Charybdis of competitive marketing, must do so to be successful … Judgment and foresight are the most essential qualities in the manager of a business enterprise … When choice must be made between a manager of great executive ability and one of exceptional foresight, the latter will be selected in a majority of instances.

Investors. Those who have capital to invest are certain to apply their utmost ability in seeking to foresee the course of prices for the commodity or security in which they are interested … it is frequently difficult to distinguish between the investor and the unmixed speculator.

Speculators. That a considerable portion of the population is either permanently or temporarily identified with this class is a fact as well known as it is regrettable.

Selden (1902) concluded that even in the simplest consumptive purchases the element of foresight is frequently present and that the effort to speculate, for the most part unrecognized and often almost unconscious, and its temporary effect upon demand practically indistinguishable from actual consumption, permeates in varying degrees the entire social structure. The action of the investor tends to lessen fluctuations and is usually beneficial both to himself and to society as a whole, while the action of the gambler tends to widen fluctuations and is invariably injurious both to himself and to society. Selden’s gambler is equivalent to short-selling traders of twenty-first century.

Size of the scheme

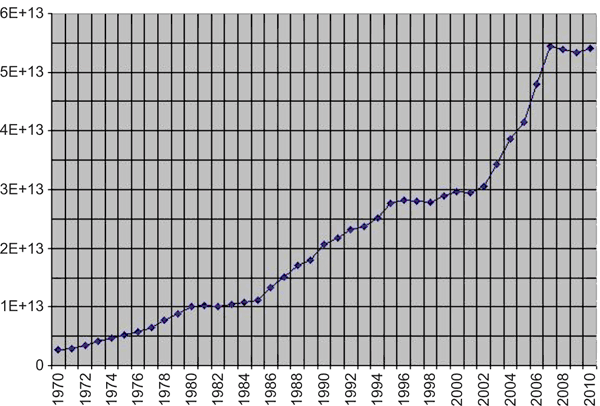

World gross product was US$54.3 trillion in 2007. The increase in world gross product between 2002 and 2007 (Figure 1) should have rung alarm bells at the World Bank, IMF and governmental regulatory agencies.

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Emerald | The Trouble with Markets – Saving Capitalism from Itself

Figure 1 World gross product

During the same period the size of the credit derivatives industry reached US$ 58 trillion with no regulation; credit-default swap market size reached US$ 27 trillion (Wall Street Journal – Europe, 2009d). Kessler (2009) estimated the market size for credit derivatives as US$62 trillion. Despite all these problems, Mr Trichet of European Central Bank did not distance himself from his longer-standing view that financial technology has been beneficial for economic growth world-wide although he admits that the interactions of perverse incentives, excessive complexity and global imbalances, threw the credit boom into reverse (Wall Street Journal – Europe, 2009g). Roger Bootle defends this financial technology, too.

Financial institutions and investors worldwide are reported to ultimately realize US$2 trillion in losses on US loans, but recognized only half of those losses so far (Wall Street Journal – Europe, 2009c). I venture to forecast that the actual figure will lie somewhere between US$3.1 trillion and US$5.4 trillion.

Apparently, during the financial markets turmoil, stocks all over the world lost US$ 30 trillion in value, whereas home equity dropped US$11 trillion. But, we need to know the number of transactions at each price level and compare them with the original purchase price to determine the actual losses. Most of the losses could be “paper-loss”. The author details beautifully the schemes employed by the financial actors in USA to cheat the system.

It is difficult to understand how governments, IMF and World Bank did/do not see that the amount of free-floating financial capital in 2009 is much larger than its amount in 1950 or 1970 or 1990! When the vast amount of free-floating financial capital ends in the hands of speculators, there is no way of escaping the crisis.

Roger Bootle is against the proposal that financial company size should be capped to get rid of “too-big-too-fail” cases, although the “Big Bang” architects in UK did question in 2009 the ideal of unfettered capitalism on which it was built. Under former Prime Minister Margaret Thatcher, a small group of officials, including Treasury chief Nigel Lawson and Secretary of State for Trade and Industry Cecil Parkinson, scrapped decades-old rules at the stock exchange and other institutions. Looking back two decades later, Messrs Lawson and Parkinson say at least one thing went wrong: Banks were allowed to grow too big for anyone, including their own managers, to oversee. At the end of 2008, UK bank assets amounted to US$11.31 trillion, ca. four times the size of the UK economy (2008 GDP US$2.79 trillion)!! One sees that

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Emerald | The Trouble with Markets – Saving Capitalism from Itself

governments have little choice but to bail them out when they get into trouble(Wall Street Journal – Europe, 2009e). The case of Ireland is a perfect example, where the Irish government has guaranteed bank liabilities of US$ 632 billion, more than twice GDP (Wall Street Journal – Europe, 2009b).

Governments are part of the Worldwide PONZI Scheme as the following stories tell us. The pharmaceutical company Eli Lilly & Co agreed to pay US$ 1.42 billion to US Justice Department to settle a probe into alleged improper marketing of the antipscyhotic drug Zyprexa (Henninger, 2009b). UK Financial Services Authority fined a unit of US Insurance Broker AonCorp US$ 7.9 million for weak controls on payments made overseas that could be used for bribes in Bahrain, Bangladesh, Bulgaria, Indonesia, Mynamar, Vietnam (Wall Street Journal – Europe, 2009a). Why are US Administration and UK Government making money when US companies misbehave?

Countries hold US$11 trillion as central bank reserves, mostly in US government papers; individuals in Turkey hold twice the Central Bank reserves as US$ deposit. A naive estimate would claim that individuals in all countries are holding US$22 trillion.

US government debt has reached US$ 11 trillion and expected to reach US$13 trillion within two years. US government spends US$3 trillion in an economy of US$14.3 trillion (2008 GDP); there were 19 million empty houses repossessed by banks in USA at the end of 2008; total commercial real-estate loans outstanding in USA at the end of 2008 is ca. US$1.70 trillion. The financial products unit of AIG in USA holds US$1.6 trillion derivatives portfolio (Wall Street Journal – Europe, 2009d). Bank of America holds US$ 1 trillion deposits, one may wonder on their whereabouts! The private equity firms in USA have more than US$1 trillion available for deal making. Guess whose money this could be! On page 3, the author says that “[…] the fortunes ‘earned’ by bankers high and low were not really earned, but expropriated from the rest of us”.

US pharmaceutical and technology companies hold US$250 billion in cash and have US$220 billion debt. A total of 55 million vehicles were sold worldwide in 2007, 16 million in the USA; this figure dropped to ca. 13 million in the USA in 2008 and is expected to hover around 9 million in 2009.

The Japanese companies sit on US$1.5 trillion cash; Government debt-to-GDP in Japan is 157 percent according to Japanese government, but 180 percent according to OECD (Wall Street Journal – Europe, 2009f) and will reach 200 percent in 2010, risking a downgrading in country credit rating.

Conclusions

The USA is at the apex of the Worldwide PONZI Scheme. Efforts are under way to add layers to the bottom of the pyramid by luring Russia, China, India and African countries into the scheme, before “[…] if we are not careful, the fall of finance capitalism could bring the whole superstructure crashing down on our heads” (page 92). Reshuffling world economy could put another country at the apex of the Worldwide PONZI Scheme, which would probably be prevented from materializing by a war (a foresight!).

Let us remember Schumpeter from 1928: “Capitalism, whilst economically stable, and even gaining in stability, creates, by rationalizing the human mind, a mentality and a style of life incompatible with its own fundamental conditions, motives and social institutions, and will be changed, although not by economic necessity and probably even at some sacrifice of economic welfare, into an order of things […]”

Bootle concludes on page 251 “Regardless of who ‘got it right’ in the past, it is now imperative that the world ‘gets it right’ for the future.” To realize this we need to find “a way of ensuring that independently acting individuals may simultaneously enjoy correct foresight” (Coddington, 1982).

Bootle’s book could be a starter for interested individuals for survival in this world, as it covers many important topics of economics and management fields.

M. Atilla Öner Chairman of the Board of Directors, Yeditepe University Management Application and Research Center, Istanbul, Turkey References

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Emerald | The Trouble with Markets – Saving Capitalism from Itself

Coddington, A. (1982), “Deficient foresight: a troublesome theme in Keynesian economics”, The American Economic Review, Vol. 72 No. 3, pp. 480–7 (The) Economist (2009), “A Ponzi scheme that works”, December 19, p. 69 Gore, A. Jr (1985), “Government foresight: an investment for the future”, Planning Review, November, pp. 30–2 Gort, M. and Wall, R.A. (1988), “Foresight and public utility regulation”, The Journal of Political Economy, Vol. 96 No. 1, pp. 177–88 Gottheil, F.M. (1999), Principles of Microeconomics, 2nd ed. , South-Western College PublishingCincinnati, OH, p. 408 Henninger, D. (2009a), Wall Street Journal – Europe, January 8 Henninger, D. (2009b), Wall Street Journal – Europe, March 16, p. 31 Kessler, A. (2009), Wall Street Journal – Europe, March 27-29 Mitchell, W.C. (1914), “Human behavior and economics: a survey of recent literature”, The Quarterly Journal of Economics, Vol. 29 No. 1, pp. 1–47 Oberdiek, H. (1972), “Intention and foresight in criminal law”, Mind, New Series, Vol. 81 No. 323, pp. 389–400 Schumpeter, J. (1928), “The instability of Capitalism”, The Economic Journal, Vol. 38 No. 151, pp. 361–86 Selden, G.C. (1902), “Trade cycles and the effort to anticipate”, The Quarterly Journal of Economics, Vol. 16 No. 2, pp. 293–310 Steigerwald, D.G. and Stuart, C. (1997), “Econometric estimation of foresight: tax policy and investment in the United States”, The Review of Economics and Statistics, Vol. 79 No. 1, pp. 32–40 Wall Street Journal – Europe (2009a), January 9 Wall Street Journal – Europe (2009b), January 16-18 Wall Street Journal – Europe (2009c), January 19 Wall Street Journal – Europe (2009d), March 19 Wall Street Journal – Europe (2009e), March 31 Wall Street Journal – Europe (2009f), April 1 Wall Street Journal – Europe (2009g), April 28 Watling, J. (1964), “Book review: Foresight and Understanding by Stephen Toulmin”, The British Journal for the Philosophy of Science, Vol. 15 No. 58, pp. 164–6

http://www.emeraldinsight.com/journals.htm?issn=1463-6689&volume=12&issue=4.

Eficacia analgésica y tolerancia de piroxicam/ ß-ciclodextrina comparado con piroxicam, paracetamol y placebo en el tratamiento del dolor post extracción dental. Introducción Resultados Los grupos de tratamiento eran homogéneos tanto por las E l dolor postoperatorio agudo es una experiencia común en la características demográficas de los pacientes como por la

Opening of the 12th Annual Sir Arthur Lewis Institute of Social and Economic Studies Conference 23 March 2011 Brian Wynter What’s in Your Wallet? Thank you for inviting me to this gathering of minds meeting here to consider what we have done with our political and economic freedom since Independence, what we should learn from Coming to a shared vision of the future is one t

Emerald | The Trouble with Markets – Saving Capitalism from Itself

The Trouble with Markets – Saving Capitalism from Itself

Emerald | The Trouble with Markets – Saving Capitalism from Itself

The Trouble with Markets – Saving Capitalism from Itself  Emerald | The Trouble with Markets – Saving Capitalism from Itself

Figure 1 World gross product

Emerald | The Trouble with Markets – Saving Capitalism from Itself

Figure 1 World gross product